➡️ INTRODUCTION

➡️ Farmer pension schemes are government-backed initiatives designed to provide financial security to farmers after retirement. Farming is a labor-intensive occupation with uncertain income due to climate, market fluctuations, and crop failures. These pension schemes ensure that farmers have a steady source of income in their later years, reducing financial stress and dependency on family. The schemes are tailored for small and marginal farmers, offering them regular monthly pensions after reaching the eligible age. Apart from financial stability, these programs also encourage farmers to save systematically during their active farming years. Understanding eligibility criteria, benefits, and application processes is essential for farmers to take full advantage of these schemes and secure a better future.

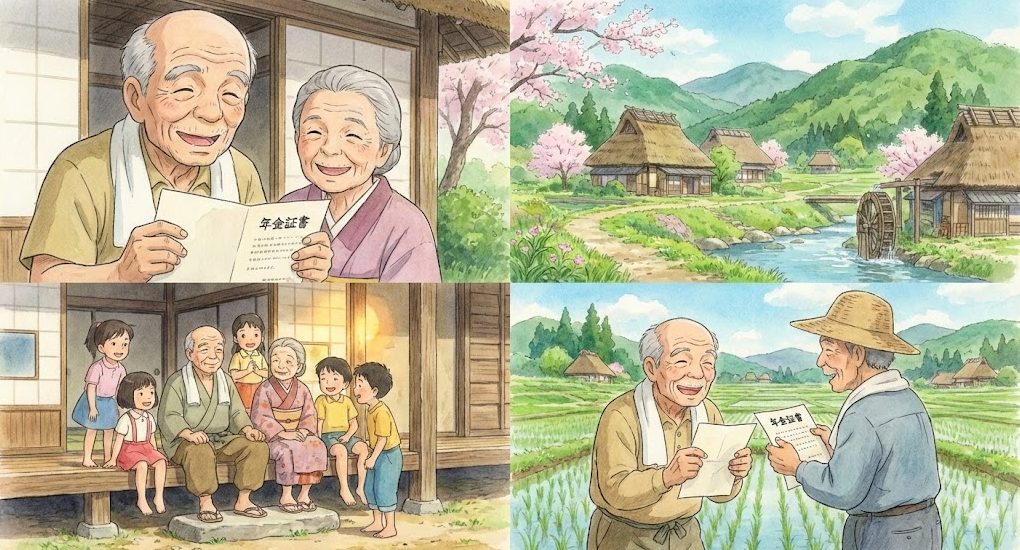

➡️ Pension schemes provide financial security to retired farmers.

➡️ They reduce dependency on family members after old age.

➡️ Regular contributions help in accumulating a substantial retirement corpus.

➡️ Awareness about schemes ensures eligible farmers do not miss out on benefits.

➡️ Government-backed programs make the process reliable and accessible.

➡️ Below are the key points that explain eligibility, benefits, and the application process for farmer pension schemes.

🔵 1️⃣ ➡️ Eligibility Criteria for Farmers

➡️ To apply for a farmer pension scheme, individuals must meet specific eligibility criteria. Generally, applicants should be small or marginal farmers owning or cultivating land within the prescribed limits. Age criteria usually require farmers to be between 18 and 40 years at the time of enrollment, depending on the scheme. Some programs also mandate that the farmer must be a resident of the state where the scheme is offered. Accurate documentation, such as land records, identity proof, and bank account details, is necessary to verify eligibility. Meeting these requirements ensures smooth enrollment and avoids rejection of applications. Farmers should also ensure they are not enrolled in duplicate pension schemes to comply with government regulations.

🔵 2️⃣ ➡️ Contribution and Payment Structure

➡️ Farmer pension schemes operate on a contribution-based system where farmers deposit a fixed amount regularly. Contributions can be monthly, quarterly, or yearly, depending on the scheme. The government may co-contribute a percentage of the deposit to encourage participation. The total accumulated contribution along with interest determines the pension amount after retirement. Payment options often include online transfers to registered bank accounts to ensure transparency and efficiency. Consistent contributions are crucial to maximize benefits, as irregular payments may reduce the final pension. Understanding the payment structure helps farmers plan their finances better and ensures they can sustain regular contributions until retirement.

🔵 3️⃣ ➡️ Pension Benefits and Amount

➡️ The primary benefit of farmer pension schemes is a guaranteed monthly pension after attaining the eligible age, usually 60 years. The amount depends on the total contributions, tenure of participation, and applicable interest rates. Some schemes also provide additional benefits like accidental death coverage, spouse pension, or lump-sum payment at the time of retirement. Receiving a regular pension helps farmers cover daily expenses, medical costs, and unforeseen emergencies. Besides financial support, these pensions offer peace of mind, knowing that they are protected in old age. Farmers can calculate expected pension using online calculators provided by many schemes, aiding in better financial planning.

🔵 4️⃣ ➡️ Application Process for Enrollment

➡️ The application process for farmer pension schemes is designed to be simple and accessible. Farmers can enroll through designated government offices, online portals, or banking partners. The process requires submission of personal details, land ownership proof, identity verification, and bank account information. Some states also allow self-registration via mobile applications. After verification, applicants receive a unique enrollment number, and contribution schedules are shared. Timely submission of documents and verification is essential to avoid delays in enrollment. Farmers are advised to keep copies of all submitted documents and receipts as proof of enrollment and contributions. Proper understanding of the application process ensures smooth entry into the pension program.

🔵 5️⃣ ➡️ Awareness and Support Services

➡️ Awareness about farmer pension schemes is vital for maximizing participation and benefits. Governments often conduct workshops, awareness drives, and distribution of informational material to educate farmers about scheme features, eligibility, and application steps. Helpline numbers, online chat support, and local agriculture offices provide guidance for troubleshooting issues. Farmers can also seek help from community groups or cooperatives for understanding contribution calculations and submission processes. Staying informed ensures that eligible farmers do not miss enrollment opportunities and can benefit fully from government support. Continuous support and awareness initiatives enhance trust and transparency in these pension programs.

➡️ CONCLUSION

➡️ Farmer pension schemes play a critical role in providing financial stability and security to retired farmers. By understanding eligibility criteria, contribution structures, benefits, and the application process, farmers can plan effectively for their post-retirement life. Regular contributions, timely enrollment, and awareness of available support services ensure that farmers receive consistent pensions and additional benefits like accidental coverage or spouse pensions. These schemes not only reduce financial dependence but also improve the quality of life for senior farmers. Adopting a disciplined approach toward pension contributions and staying informed about government programs allows farmers to enjoy a secure and dignified retirement.